Your credit score is a critical part of your financial health – it influences everything from the interest rates you qualify for when you borrow money to your ability to secure a mortgage or payday loan. So, when you notice a sudden drop in your credit score, it can be a cause for concern and confusion.

In this article, we’ll explore some common reasons why your credit score may have taken a hit and what steps you can take to address the issue.

1) Missed or Late Payments

One of the most significant factors that can contribute to a drop in your credit score is missed or late payments. Payment history accounts for a significant portion of your credit score, and any instances of payments being 30 days or more past due can have a negative impact. This includes missing payday loan payments which can hurt your credit.

Whether it’s a credit card, mortgage, or any other type of loan, failing to make payments on time signals to creditors that you may be a risky borrower.

To address this issue, make sure to prioritize timely payments. Set up reminders or automatic payments to ensure you never miss a due date. If you’re struggling to make payments, consider contacting your creditors to discuss possible alternatives, such as adjusting your payment schedule or negotiating a temporary hardship arrangement.

2) High Credit Utilization

Credit utilization (or the ratio of your credit card balances to your credit limits), is another important factor in determining your credit score. If your credit card balances are consistently close to or at the maximum limit, it can signal financial distress to credit bureaus.

Ideally, you should aim for a credit utilization rate below 30% to maintain a positive impact on your credit score.

To address high credit utilization, consider paying down your credit card balances. This can involve creating a budget, prioritizing payments on high-interest cards, or exploring debt consolidation options. Additionally, requesting a credit limit increase or opening a new credit card (while being cautious about accumulating more debt) can help improve your credit utilization ratio.

3) Closing Old Credit Accounts

Closing old credit accounts might seem like a responsible financial move, especially if you’re looking to simplify your financial portfolio. However, this action can have unintended consequences for your credit score.

The length of your credit history is a factor in your credit score calculation, and closing old accounts can shorten the average age of your credit accounts, potentially resulting in a lower score.

Instead of closing old accounts, consider keeping them open and using them occasionally to maintain activity. Closing accounts should be done strategically and only after careful consideration of the potential impact on your credit score.

4) Credit Report Errors

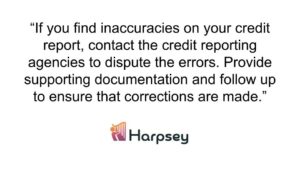

It is not uncommon for errors to occur on your credit report. Inaccurate information on your credit report, such as accounts that don’t belong to you, incorrect payment statuses, or outdated information, can negatively impact your credit score.

Regularly reviewing your credit report is essential to catch and dispute any errors promptly.

If you find inaccuracies on your credit report, contact the credit reporting agencies to dispute the errors. Provide supporting documentation and follow up to ensure that corrections are made. Monitoring your credit report regularly can help you catch and address errors before they significantly impact your credit score.

Maintaining a good credit score requires you to be vigilant and have responsible financial habits. If you’ve noticed a drop in your credit score, don’t panic. Instead, carefully review your financial habits, identify the potential causes and take proactive steps to address the issues.

By understanding the factors that influence your credit score, you can take control of your financial well-being and work towards improving your creditworthiness over time.